AML screening South Africa

Comprehensive anti-money laundering screening for South African businesses. PEP screening, sanctions list checks, adverse media monitoring, and watchlist screening - all in one platform for FICA compliance.

1. What is AML Screening?

AML (Anti-Money Laundering) screening is the process of checking individuals and entities against various watchlists, sanctions lists, and databases to identify potential money laundering, terrorist financing, or other financial crime risks.

In South Africa, AML screening is a legal requirement under FICA for all Schedule 1 accountable institutions. Failure to conduct proper AML screening can result in significant penalties, criminal prosecution, and reputational damage.

Why AML Screening Matters

- Prevent money laundering through your business

- Combat terrorist financing

- Meet FICA compliance requirements

- Avoid penalties up to R100 million

- Protect your business reputation

2. Types of AML Screening

Sanctions Screening

Screen against international and local sanctions lists to identify prohibited individuals and entities.

Lists & Sources Checked:

- UN Security Council consolidated list

- OFAC Specially Designated Nationals (SDN)

- EU consolidated sanctions list

- UK HM Treasury sanctions

- South African targeted financial sanctions

- FATF high-risk jurisdictions

Compliance: Required under FICA for all accountable institutions

PEP Screening

Identify Politically Exposed Persons who require enhanced due diligence.

Lists & Sources Checked:

- Domestic PEPs (South African government officials)

- Foreign PEPs (foreign government officials)

- International organization officials

- Family members of PEPs

- Close associates of PEPs

- Former PEPs (high-risk period)

Compliance: FICA Section 21A mandates EDD for all PEPs

Adverse Media Screening

Monitor news and media sources for negative information about customers.

Lists & Sources Checked:

- Financial crime mentions

- Fraud allegations

- Corruption cases

- Regulatory actions

- Criminal proceedings

- Reputational concerns

Compliance: Part of enhanced due diligence under FIC guidance

Watchlist Screening

Check against law enforcement and regulatory watchlists.

Lists & Sources Checked:

- Interpol wanted persons

- FBI most wanted

- Domestic law enforcement lists

- Regulatory enforcement actions

- Debarred parties lists

- Industry-specific blacklists

Compliance: Supports comprehensive risk assessment

3. FICA Requirements

FICA mandates comprehensive AML procedures for all accountable institutions:

Section 21: Customer Due Diligence

Verify customer identity and assess risk profile including AML screening.

Section 21A: Enhanced Due Diligence

Apply additional scrutiny for PEPs and high-risk customers including ongoing AML monitoring.

Section 28: Cash Threshold Reporting

Report cash transactions ≥R24,999.99 to the FIC.

Section 29: Suspicious Transaction Reporting

File STRs for suspected ML/TF within 15 days of forming suspicion.

Section 28A: Terrorist Property Reporting

Report property associated with terrorist activity immediately.

Section 42: RMCP

Maintain risk management and compliance programme including AML procedures.

Penalties for Non-Compliance

Failure to comply with FICA AML requirements can result in administrative penalties up to R10 million, criminal prosecution with fines up to R100 million and imprisonment up to 15 years for money laundering offences.

4. How AML Screening Works

Submit Customer Data

Enter customer name, date of birth, ID number, and other identifying information.

Database Matching

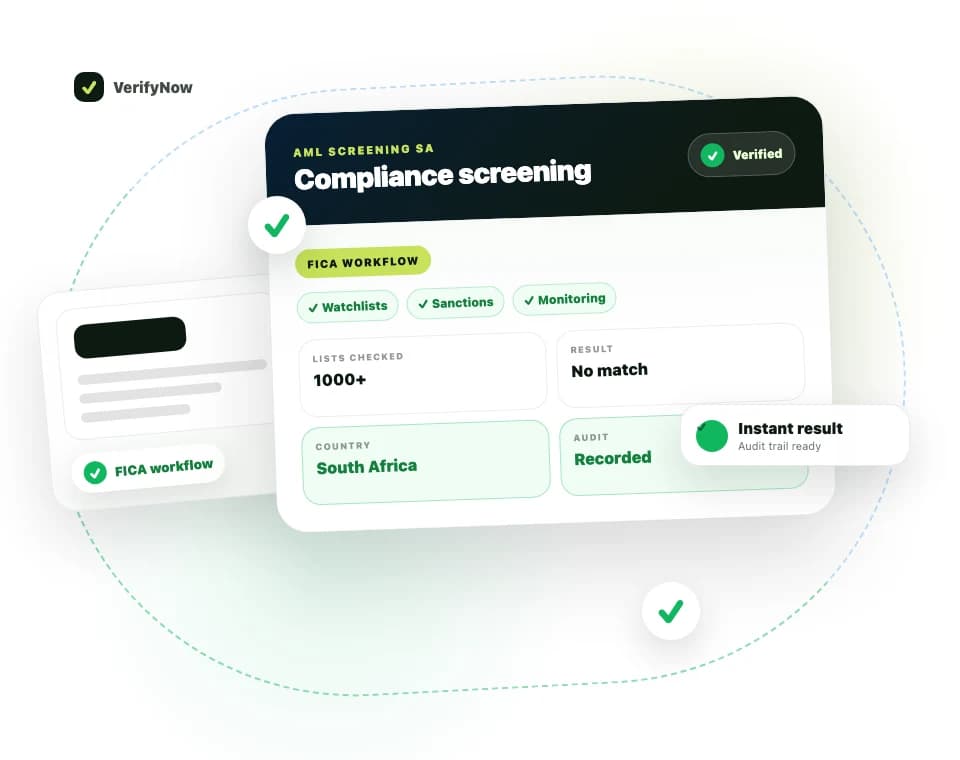

System checks against 1000+ watchlists, sanctions lists, and PEP databases using fuzzy matching algorithms.

Match Analysis

Potential matches are analyzed and scored based on match quality and relevance.

Result Review

Review matches and determine if they are true positives requiring action or false positives to be cleared.

Case Resolution

Document your decision and any actions taken. True matches may require EDD, STR filing, or relationship termination.

Ongoing Monitoring

Continuous screening alerts you when a customer appears on a watchlist after onboarding.

5. AML Red Flags

Watch for these warning signs that may indicate money laundering or terrorist financing:

6. Benefits of Automated AML

Automated Screening

Instant results against global databases

Continuous Monitoring

Ongoing screening for list updates

Fuzzy Matching

Catches name variations and aliases

Full Audit Trail

Complete records for compliance

Run from your dashboard

No code required — type a name and ID, get the risk outcome in seconds

Case Management

Workflow for match resolution

7. Frequently Asked Questions

What is AML screening?

AML (Anti-Money Laundering) screening is the process of checking customers against watchlists, sanctions lists, and PEP databases to identify potential money laundering or terrorist financing risks. In South Africa, AML screening is required under FICA for all accountable institutions.

What sanctions lists are checked in AML screening?

Comprehensive AML screening checks multiple sanctions lists including: UN Security Council sanctions, OFAC (US Treasury), EU consolidated list, UK HM Treasury sanctions, South African targeted financial sanctions, and various other government watchlists. Additional screening includes PEP databases and adverse media sources.

Who needs to conduct AML screening in South Africa?

Under FICA, all Schedule 1 accountable institutions must conduct AML screening. This includes banks, insurance companies, estate agents, attorneys, accountants, casino operators, motor vehicle dealers, and others. AML screening is particularly important for PEPs and high-risk customers requiring enhanced due diligence.

How often should AML screening be conducted?

AML screening should be conducted at customer onboarding and then on an ongoing basis. Best practice is to screen customers against updated lists at least monthly for high-risk customers, quarterly for medium-risk, and annually for low-risk. Transaction monitoring should be continuous.

What is PEP screening?

PEP (Politically Exposed Person) screening identifies individuals who hold or have held prominent public positions, as well as their family members and close associates. PEPs are considered higher risk for money laundering due to their access to public funds and influence. FICA Section 21A requires enhanced due diligence for all PEPs.

Related Resources

Start AML screening today

VerifyNow provides comprehensive AML screening against 1000+ watchlists, PEP databases, and sanctions lists. Instant results with full audit trail for FICA compliance.